Refinancing a Car Lease: Is It Possible?

Understanding Car Lease Refinancing Options and Possibilities

So, you're wondering if you can refinance a car lease? It's a fair question! Most people think of refinancing with car *loans*, but leases are a different beast. The short answer is: it's usually not possible to *refinance* a car lease in the traditional sense. You can't just walk into a bank and get a lower interest rate on your existing lease. The lease agreement is between you and the leasing company (usually the car manufacturer's financial arm), and they're generally not open to renegotiating the terms mid-lease.

However, don't despair! There *are* ways to potentially lower your monthly payments or get out of your lease early. Let's explore these alternatives:

Lease Buyout: An Alternative to Traditional Refinancing for Car Leases

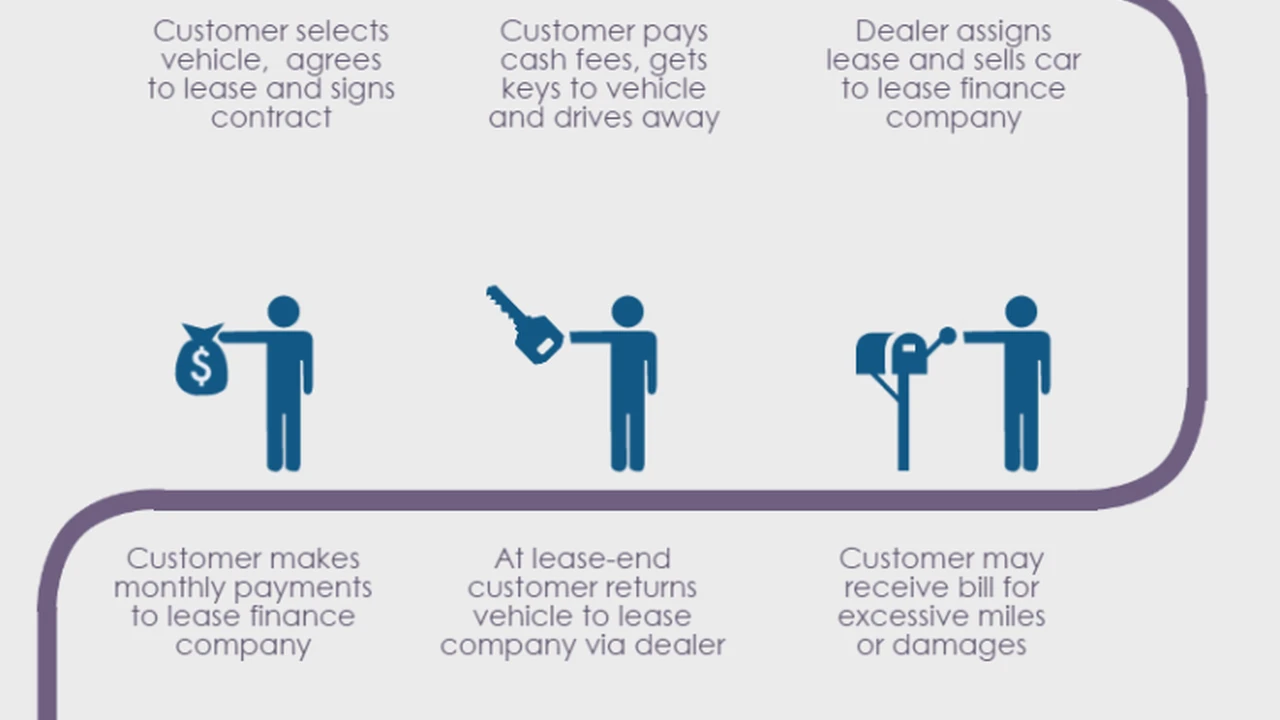

One option is a lease buyout. This essentially means you're purchasing the car from the leasing company. At the end of your lease (or sometimes even before), the leasing company will give you a buyout price. This price is usually based on the car's estimated market value at that point, plus any remaining lease payments and fees.

Now, *this* is where refinancing comes in. You can't refinance the lease itself, but you *can* refinance the loan you take out to buy the car. So, if the buyout price is, say, $15,000, you could apply for a car loan for $15,000. If you can find a loan with a lower interest rate than what's implied in your original lease, you could potentially save money each month.

When to Consider a Lease Buyout and Refinance:

- You love the car and want to keep it.

- The buyout price is lower than the car's market value. Do some research on sites like Kelley Blue Book or Edmunds to see what similar cars are selling for.

- You can secure a car loan with a significantly lower interest rate than what you're effectively paying on the lease.

Lease Transfer: Transferring Your Car Lease Responsibility

Another option is a lease transfer, also known as a lease assumption. This involves finding someone else to take over your lease. Basically, they step into your shoes and make the remaining payments. Several websites specialize in facilitating lease transfers, such as LeaseTrader.com and Swapalease.com.

Benefits of a Lease Transfer:

- You can get out of your lease early without paying hefty early termination fees.

- The new lessee gets a shorter-term lease with potentially lower monthly payments than a new lease.

Things to Consider with Lease Transfers:

- Your leasing company needs to approve the transfer. They'll typically run a credit check on the potential new lessee.

- You might be responsible for a transfer fee.

- You might still be liable if the new lessee defaults on the payments (although this varies by leasing company). Read the fine print carefully!

Early Lease Termination: Understanding the Costs

The least desirable option is usually early lease termination. This involves returning the car to the leasing company before the end of the lease term. However, this almost always comes with significant penalties. These penalties can include:

- The remaining lease payments

- Early termination fees

- Disposition fees (fees for preparing the car for resale)

- The difference between the car's market value and the residual value (the value the leasing company estimated the car would be worth at the end of the lease)

Early termination can be very expensive, so it's generally best to explore other options first.

Negotiating with the Leasing Company: Exploring Your Options

It's always worth talking to the leasing company directly. Explain your situation and see if they're willing to work with you. They might be able to offer a reduced payment plan or other concessions, especially if you're facing financial hardship.

Car Lease Refinancing and Credit Scores: The Importance of a Good Credit Score

Whether you're considering a lease buyout and refinance or trying to get approved for a lease transfer, your credit score is crucial. A good credit score will help you qualify for a lower interest rate on a car loan (for the buyout) and increase your chances of finding someone to take over your lease (as the leasing company will be more likely to approve the transfer).

Check your credit score regularly and take steps to improve it if necessary. Pay your bills on time, keep your credit utilization low (the amount of credit you're using compared to your total available credit), and avoid opening too many new credit accounts at once.

Specific Product Recommendations for Lease Buyout Refinancing and Car Ownership

Okay, so you're leaning towards a lease buyout and refinancing? Great! Here are a few specific loan products and services to consider. Remember to shop around and compare rates and terms before making a decision. These are examples, and rates and availability may vary.

LightStream Auto Loans: Unsecured Loan Option for Car Lease Buyouts

LightStream is a division of Truist Bank and offers unsecured auto loans, which can be a good option for a lease buyout. Unsecured means you don't use the car itself as collateral. This can be advantageous in some situations. They are known for competitive rates, especially for borrowers with excellent credit. They also offer a rate beat program (check their website for details). Loan amounts typically range from $5,000 to $100,000, making them suitable for most lease buyouts.

Use Case: Imagine you've leased a Honda Accord and the buyout price is $18,000. You have excellent credit (750+). LightStream could offer you an unsecured loan at a competitive rate, potentially lower than what you'd get at a traditional dealership. You use the loan to buy the Accord and now own it outright.

Pros: Competitive rates for excellent credit, unsecured loan option, no origination fees.

Cons: Requires excellent credit, unsecured loans often have slightly higher rates than secured loans.

Pricing: Interest rates vary based on creditworthiness but are generally very competitive. Check LightStream's website for current rates.

Capital One Auto Navigator: Simplifying the Car Loan Process for Lease Buyouts

Capital One Auto Navigator allows you to pre-qualify for a car loan online without impacting your credit score. This is a fantastic tool for understanding your potential interest rates and loan amounts before you even start shopping for a car (or in this case, buying out your lease). They work with a large network of dealerships, but you can also use the pre-qualification to shop for a loan elsewhere.

Use Case: You're considering buying out your BMW 3 Series lease. You use Capital One Auto Navigator to get pre-qualified for a loan. You see that you're approved for a $25,000 loan at a 4.5% interest rate. This gives you a benchmark to compare against other loan offers.

Pros: Pre-qualification without impacting credit score, large network of dealerships, user-friendly online platform.

Cons: Interest rates may not be the absolute lowest available, requires some online research.

Pricing: Interest rates vary based on creditworthiness. Check Capital One Auto Navigator for pre-qualification and potential rates.

Local Credit Unions: Personalized Service and Competitive Loan Rates for Car Lease Buyouts

Don't overlook your local credit unions! Credit unions often offer very competitive interest rates and more personalized service than larger banks. They are member-owned, so they often prioritize the needs of their members. You'll need to become a member to get a loan, but the requirements are usually straightforward (e.g., living or working in a specific area).

Use Case: You're looking to buy out your Toyota RAV4 lease. You join a local credit union in your area. They offer you a car loan with a slightly lower interest rate than you found online, and they also provide more personalized advice and support throughout the loan process.

Pros: Competitive interest rates, personalized service, member-owned structure.

Cons: Requires membership, may have stricter eligibility requirements than some online lenders.

Pricing: Interest rates vary. Contact your local credit unions for specific rates and terms.

Comparing Car Lease Buyout Refinancing Options: Making the Right Choice

When comparing these options, consider the following factors:

- Interest Rate: The lower the interest rate, the less you'll pay over the life of the loan.

- Loan Term: A shorter loan term means higher monthly payments but less interest paid overall. A longer loan term means lower monthly payments but more interest paid overall.

- Fees: Look for loans with no origination fees, prepayment penalties, or other hidden fees.

- Credit Score Requirements: Make sure you meet the credit score requirements for the loan.

- Loan Amount: Ensure the loan amount is sufficient to cover the buyout price of your lease, plus any taxes and fees.

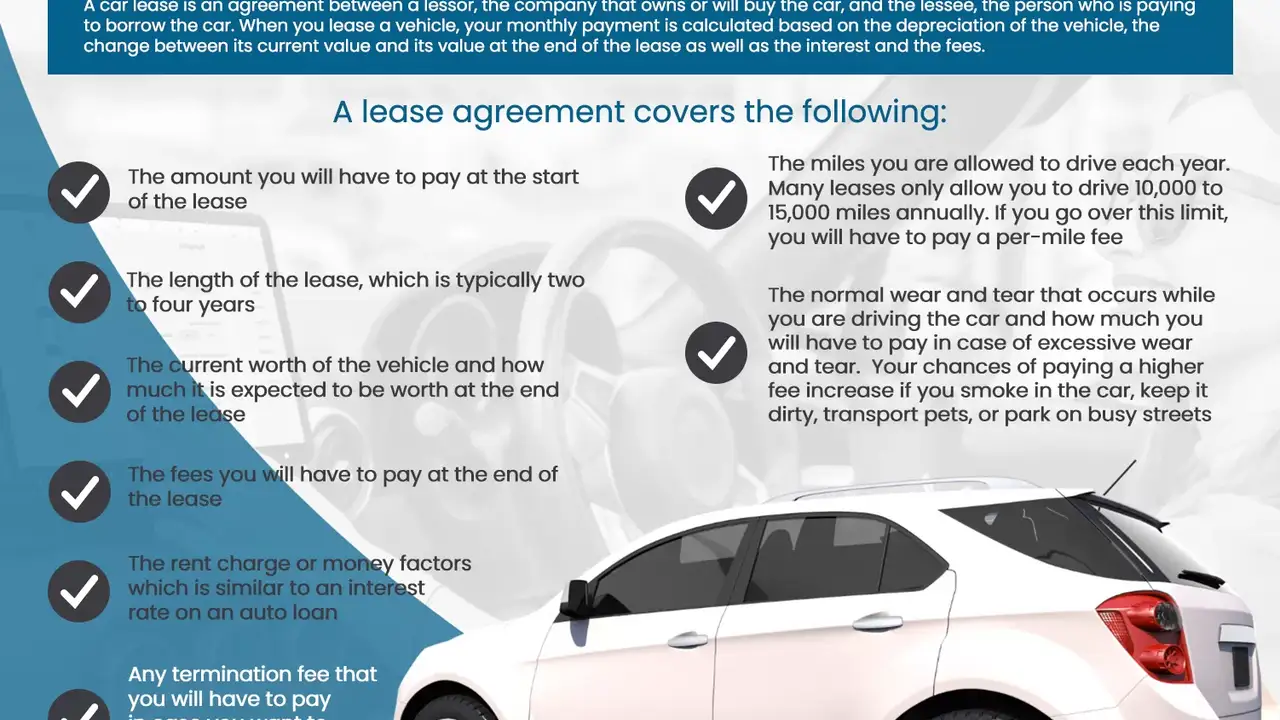

Understanding Car Lease Agreements: Key Terms and Conditions

Before you even consider refinancing (or any alternative), make sure you thoroughly understand your lease agreement. Pay close attention to the following:

- Mileage Allowance: What's your mileage allowance, and what are the penalties for exceeding it?

- Excess Wear and Tear Charges: What's considered "excess wear and tear," and how much will you be charged for it?

- Early Termination Fees: How much will it cost to terminate the lease early?

- Buyout Price: What's the buyout price at the end of the lease term?

- Transfer Policy: Does the leasing company allow lease transfers, and what are the requirements?

Long-Term Car Ownership Considerations After a Car Lease Buyout

Once you buy out your lease, you're responsible for all the costs associated with car ownership, including:

- Maintenance and Repairs: Budget for regular maintenance and potential repairs.

- Insurance: You'll need to maintain adequate car insurance coverage.

- Property Taxes/Registration Fees: You'll be responsible for paying annual property taxes (if applicable in your state) and registration fees.

- Depreciation: Cars depreciate in value over time. Be aware of this when deciding whether to buy out your lease.

Buying out your lease can be a good option if you love the car, the buyout price is reasonable, and you can secure a favorable loan. Just make sure you do your research, compare your options, and understand all the costs involved.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)