How to Calculate a Car Lease Payment

Understanding Car Lease Payment Components for Savvy Budgeting

Okay, so you're thinking about leasing a car. Awesome! But before you get swept away by that shiny new ride, let's break down how those lease payments are actually calculated. It's not as scary as it seems, and understanding the components will empower you to negotiate a better deal. Think of it like this: you're renting the car for a specific period, and your payments cover the depreciation (how much the car's value drops), interest (called the money factor), and any taxes or fees.

So, what goes into that monthly number you see on the lease agreement?

- Capitalized Cost (Cap Cost): This is basically the agreed-upon price of the car. It’s negotiable, so don’t be afraid to haggle!

- Residual Value: This is the estimated value of the car at the end of the lease term. The higher the residual value, the lower your monthly payments will be. It's determined by the leasing company based on projected depreciation.

- Money Factor: This is the interest rate you're paying on the lease. It's usually expressed as a small decimal, like 0.0025. To convert it to an annual interest rate, multiply it by 2400. So, 0.0025 would be 6% (0.0025 * 2400 = 6).

- Lease Term: This is the length of your lease, typically 24, 36, or 48 months.

- Fees and Taxes: These can include acquisition fees, destination charges, registration fees, and sales tax.

Step-by-Step Guide to Calculating Your Monthly Car Lease Payment with Examples

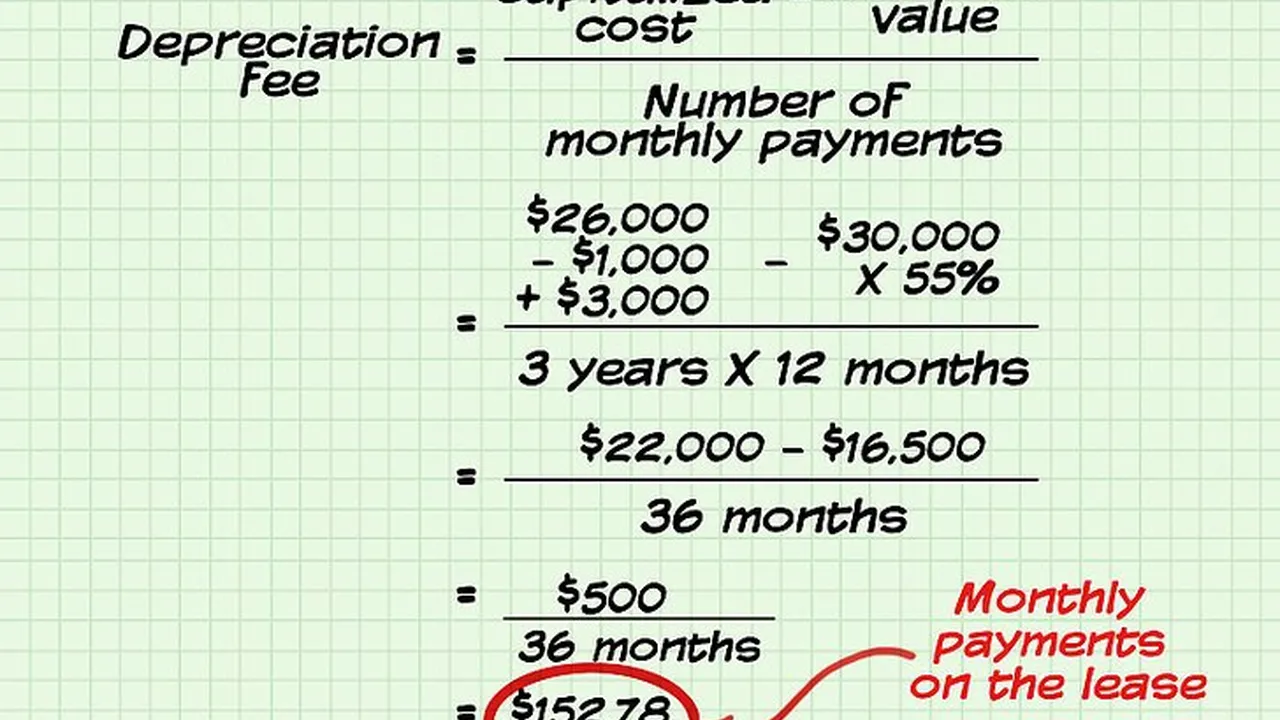

Alright, let's get into the nitty-gritty. Here's the formula for calculating your monthly lease payment:

Monthly Payment = (Depreciation + Finance Charge) + Taxes

Where:

- Depreciation = (Capitalized Cost - Residual Value) / Lease Term

- Finance Charge = (Capitalized Cost + Residual Value) x Money Factor

- Taxes = (Depreciation + Finance Charge) x Tax Rate (if applicable)

Let’s walk through an example:

Let's say you're leasing a Honda Civic.

- Capitalized Cost: $25,000

- Residual Value (after 36 months): $15,000

- Money Factor: 0.002

- Lease Term: 36 months

- Sales Tax: 6%

- Calculate Depreciation: ($25,000 - $15,000) / 36 = $277.78

- Calculate Finance Charge: ($25,000 + $15,000) x 0.002 = $80

- Calculate Taxes: ($277.78 + $80) x 0.06 = $21.47

- Calculate Monthly Payment: $277.78 + $80 + $21.47 = $379.25

So, your estimated monthly lease payment would be around $379.25.

Pro Tip: Many online lease calculators can help you with these calculations. Just search for "car lease calculator" on Google.

Negotiating the Capitalized Cost for a Lower Monthly Payment

Remember that Cap Cost we talked about? This is where your negotiation skills come in! The lower the Cap Cost, the lower your monthly payments. Treat it like buying the car outright. Research the car's market value, compare prices at different dealerships, and be prepared to walk away if you're not getting a good deal.

Here are some tips for negotiating the Cap Cost:

- Do your research: Know the car's invoice price (what the dealer paid for it).

- Shop around: Get quotes from multiple dealerships.

- Negotiate the price, not the monthly payment: Focus on the overall price of the car, not just the monthly payment. Dealers can manipulate the other factors to make the monthly payment look lower while still charging you more overall.

- Be prepared to walk away: If the dealer isn't willing to negotiate, be prepared to go to another dealership.

- Consider incentives: Ask about any incentives or rebates that you might qualify for.

Understanding and Optimizing the Residual Value in Your Car Lease

The residual value is the estimated value of the car at the end of the lease term. It's determined by the leasing company and is a key factor in calculating your monthly payments. A higher residual value means less depreciation during the lease term, resulting in lower payments.

While you can't directly negotiate the residual value, understanding it is crucial:

- Know the Market: Research the typical residual values for similar vehicles. Sites like Kelley Blue Book and Edmunds can provide estimates.

- Consider Lease Length: Shorter lease terms generally have higher residual values (because the car depreciates less).

- Choose Vehicles with Strong Resale Value: Some brands and models hold their value better than others. Research which cars tend to have higher residual values.

Decoding the Money Factor: Finding the Best Car Lease Interest Rate

The money factor is essentially the interest rate you're paying on the lease. It's usually expressed as a small decimal, like 0.0025. As mentioned before, multiply it by 2400 to get the annual interest rate (APR). A lower money factor means lower monthly payments.

Here's how to get a good money factor:

- Have Good Credit: A good credit score is essential for getting a low money factor. Check your credit report before you start shopping for a lease.

- Shop Around: Just like with the Cap Cost, get quotes from multiple dealerships. Different lenders may offer different money factors.

- Negotiate: Don't be afraid to negotiate the money factor. Point out that you have good credit and have shopped around.

- Consider a Loan Instead: Sometimes, getting a car loan and buying the car outright can be cheaper than leasing, especially if you plan to keep the car for a long time.

Hidden Car Lease Fees and Taxes: What to Watch Out For

Beyond the Cap Cost, Residual Value, and Money Factor, there are other fees and taxes that can add to the overall cost of your lease. Be sure to ask about these fees upfront and understand what they cover.

Common fees and taxes include:

- Acquisition Fee: This is a fee charged by the leasing company to cover the costs of setting up the lease.

- Disposition Fee: This is a fee charged at the end of the lease to cover the costs of preparing the car for resale.

- Destination Charge: This is the cost of transporting the car from the factory to the dealership.

- Registration Fees: These are the fees charged by your state to register the car.

- Sales Tax: This is the sales tax on the monthly lease payment.

- Excess Mileage Charges: If you drive more miles than allowed in your lease agreement, you'll be charged a per-mile fee.

- Excess Wear and Tear Charges: If the car has excessive wear and tear at the end of the lease, you'll be charged for repairs.

Tip: Read the lease agreement carefully and ask about any fees that you don't understand.

Mileage Limits and Excess Mileage Charges: Plan Your Driving Habits

Leases typically come with a mileage limit, usually between 10,000 and 15,000 miles per year. If you exceed this limit, you'll be charged a per-mile fee, which can add up quickly. Think carefully about how much you drive each year before choosing a mileage limit.

Here are some tips for managing your mileage:

- Estimate Your Annual Mileage: Track your driving habits for a few weeks to get an accurate estimate of your annual mileage.

- Choose the Right Mileage Limit: If you drive a lot, choose a higher mileage limit, even if it means a slightly higher monthly payment.

- Consider Buying Extra Miles Upfront: Some leasing companies allow you to buy extra miles upfront at a discounted rate.

- Track Your Mileage Regularly: Keep an eye on your mileage throughout the lease term so you don't get surprised by excess mileage charges at the end.

Wear and Tear Charges: Avoiding Expensive Surprises at Lease End

At the end of the lease, the car will be inspected for wear and tear. Normal wear and tear is usually acceptable, but excessive damage can result in charges. This can include things like dents, scratches, stains, and tire wear.

Here's how to avoid excessive wear and tear charges:

- Take Good Care of the Car: Keep the car clean and well-maintained.

- Repair Minor Damage: Fix any minor dents or scratches as soon as possible.

- Protect the Interior: Use seat covers and floor mats to protect the interior from wear and tear.

- Check the Tires Regularly: Make sure the tires are properly inflated and have sufficient tread.

- Review the Lease Agreement: The lease agreement will outline what is considered acceptable wear and tear.

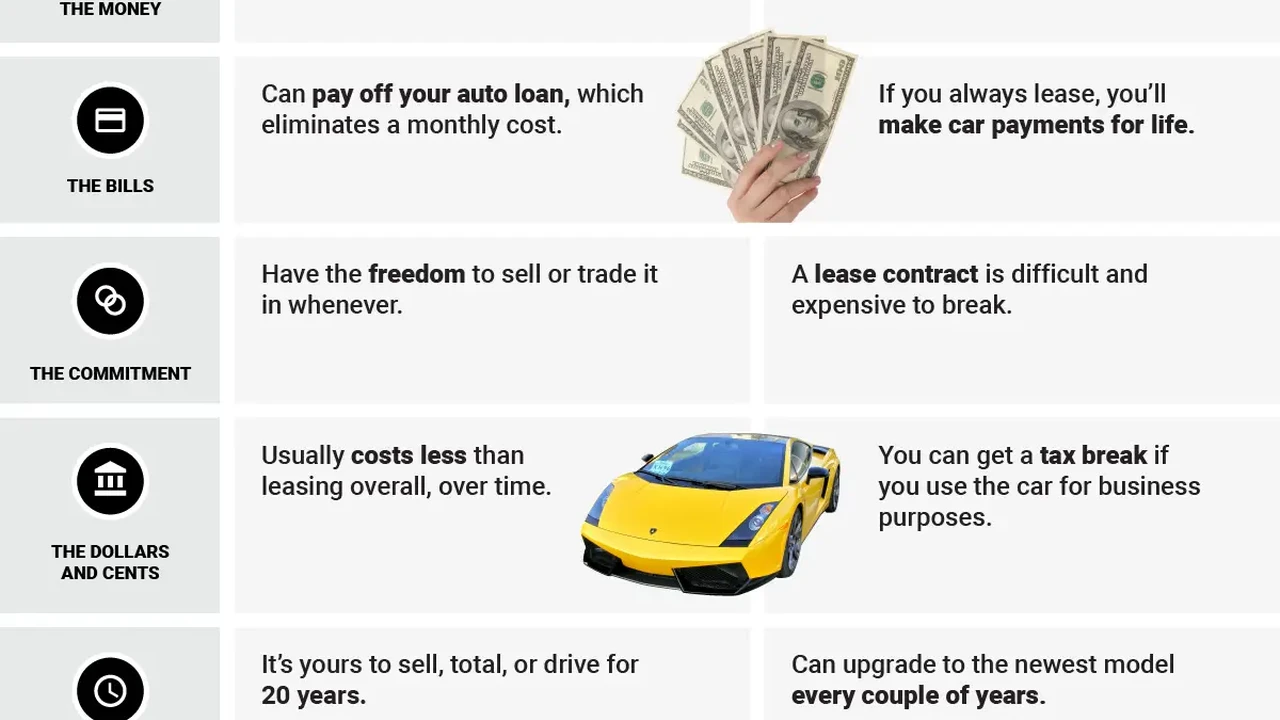

Car Lease vs Buying: Which Option Is Right for You?

Leasing and buying both have their pros and cons. Leasing can be a good option if you want to drive a new car every few years and don't want to worry about maintenance or resale value. Buying can be a better option if you plan to keep the car for a long time and want to build equity.

Here's a quick comparison:

Leasing:

- Pros: Lower monthly payments, drive a new car every few years, no worries about maintenance or resale value.

- Cons: Mileage limits, wear and tear charges, no equity, more expensive in the long run if you keep leasing.

Buying:

- Pros: No mileage limits, no wear and tear charges, build equity, cheaper in the long run if you keep the car for a long time.

- Cons: Higher monthly payments, responsible for maintenance and repairs, responsible for resale value.

Recommended Lease Deals: Top Car Models and Their Lease Prices

Okay, so you're ready to dive into the leasing world? Here are a few recommendations based on different needs and budgets. Keep in mind that lease deals change frequently, so check with your local dealerships for the most up-to-date information. Prices are estimates and will vary based on location, credit score, and incentives.

Budget-Friendly Options (Under $300/month):

- Nissan Versa: A subcompact car that's surprisingly spacious and fuel-efficient. Great for city driving. Expect a lease price around $200-$250/month with a small down payment. Ideal for students or anyone on a tight budget.

- Hyundai Elantra: A reliable and well-equipped compact sedan. Offers a good balance of value and features. Lease prices typically range from $230-$280/month. Perfect for commuters.

Mid-Range Options ($300-$450/month):

- Honda Civic: A popular and well-regarded compact car known for its reliability and fuel efficiency. Lease prices are usually in the $320-$400/month range. A great all-around choice for individuals and small families.

- Toyota Corolla: Another excellent compact car with a reputation for longevity and dependability. Similar lease prices to the Civic, around $330-$410/month. Excellent for those prioritizing reliability and resale value.

- Mazda3: A stylish and fun-to-drive compact car with a more premium feel than the Civic or Corolla. Lease prices can be a bit higher, around $350-$430/month. Suited for drivers who enjoy a sporty driving experience.

Luxury Options ($450+/month):

- BMW 3 Series: A benchmark for sporty sedans, offering a thrilling driving experience and a luxurious interior. Lease prices typically start around $480/month. Ideal for those who appreciate performance and prestige.

- Mercedes-Benz C-Class: A sophisticated and comfortable sedan with a luxurious interior and a smooth ride. Lease prices are similar to the BMW 3 Series, starting around $500/month. Perfect for drivers seeking a refined and comfortable driving experience.

- Lexus RX: A popular luxury SUV known for its reliability, comfort, and smooth ride. Lease prices generally start around $550/month. A great choice for families looking for a comfortable and reliable luxury SUV.

Real-World Car Lease Scenarios and Product Comparisons

Let's dive deeper into specific scenarios and compare some of the models mentioned above:

Scenario 1: The City Commuter

Needs: Fuel efficiency, easy parking, reliable, budget-friendly.

Best Options: Nissan Versa, Hyundai Elantra

Comparison: The Versa is the most budget-friendly option, offering excellent fuel economy and a small footprint for easy parking. However, it lacks some of the features and refinement of the Elantra. The Elantra offers a more comfortable and feature-rich experience, but at a slightly higher price. The Versa's starting MSRP is around $16,000, while the Elantra starts around $21,000. For city commuting, the Versa excels due to its maneuverability and fuel efficiency, making it ideal for navigating congested streets and minimizing fuel costs. The Elantra, while slightly larger, offers enhanced comfort and tech features for longer commutes.

Scenario 2: The Young Professional

Needs: Stylish, fun to drive, reliable, good value.

Best Options: Mazda3, Honda Civic

Comparison: The Mazda3 is the more stylish and sporty option, offering a more engaging driving experience. The Civic is known for its reliability and practicality, making it a great all-around choice. The Mazda3's interior is generally considered more upscale, while the Civic offers slightly more interior space. The Mazda3 has a starting MSRP around $22,000, and the Civic around $24,000. The Mazda3's sporty handling and stylish design make it perfect for weekend getaways and urban exploration. The Civic's reliability and practicality make it a dependable choice for daily commutes and errands.

Scenario 3: The Small Family

Needs: Spacious, comfortable, safe, reliable, good value.

Best Options: Honda Civic, Toyota Corolla

Comparison: Both the Civic and Corolla are excellent choices for small families, offering spacious interiors, comfortable rides, and strong safety ratings. The Corolla is known for its legendary reliability, while the Civic offers a slightly more engaging driving experience. Both vehicles have similar starting MSRPs, around $24,000. The Civic's slightly larger cargo area might be beneficial for families with young children. The Corolla's reputation for longevity and minimal maintenance makes it a worry-free choice for busy families.

Scenario 4: The Luxury Seeker

Needs: Luxurious, comfortable, powerful, prestigious.

Best Options: BMW 3 Series, Mercedes-Benz C-Class

Comparison: The BMW 3 Series is the sportier and more performance-oriented option, offering a thrilling driving experience. The Mercedes-Benz C-Class is more luxurious and comfortable, providing a smoother and more refined ride. Both vehicles offer high-quality interiors and advanced technology features. The BMW 3 Series has a starting MSRP around $43,000, and the Mercedes-Benz C-Class around $46,000. The BMW 3 Series' sharp handling and powerful engine make it perfect for spirited driving. The Mercedes-Benz C-Class' luxurious interior and comfortable ride make it ideal for long road trips.

Car Lease Negotiation Tactics: Getting the Best Possible Deal

Negotiating a car lease can be intimidating, but with the right knowledge and tactics, you can get a great deal. Here are some tips:

- Do Your Research: Know the car's invoice price, the residual value, and the money factor.

- Shop Around: Get quotes from multiple dealerships.

- Negotiate the Cap Cost: This is the most important factor in determining your monthly payment.

- Negotiate the Money Factor: Aim for a low money factor.

- Be Prepared to Walk Away: If you're not getting a good deal, be prepared to go to another dealership.

- Consider Incentives: Ask about any incentives or rebates that you might qualify for.

- Read the Fine Print: Carefully review the lease agreement before signing anything.

Car Lease Termination Options: What Happens If You Need to End Your Lease Early?

Sometimes, life happens, and you might need to end your lease early. This can be costly, but there are a few options:

- Early Termination: This involves paying a penalty, which can be substantial.

- Lease Transfer: You can transfer your lease to another person.

- Buyout: You can buy the car outright.

Each option has its own pros and cons, so carefully consider your situation before making a decision.

Understanding Car Lease Insurance Requirements

Leasing companies typically require you to maintain comprehensive and collision insurance coverage. The minimum coverage amounts may be higher than what's required for a purchased vehicle. Be sure to check with your insurance company and the leasing company to understand the specific requirements.

Electric Car Leases: Understanding the Incentives and Tax Credits

Leasing an electric car can be a great way to try out electric vehicle technology and take advantage of government incentives and tax credits. These incentives can significantly reduce the cost of leasing an electric car. Research the available incentives in your area before making a decision.

Final Thoughts on Car Lease Payment Calculations

Understanding how car lease payments are calculated is essential for getting a good deal. By knowing the components of the lease payment and how to negotiate them, you can save money and drive the car of your dreams.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)